Fillable Form Profit and Loss Statement

A Profit and Loss Statement is a financial document that companies use to evaluate their financial status within a time period. It enables businesses to assess their financial performance.

What is a Profit and Loss Statement?

A Profit and Loss Statement is a financial document that companies use to evaluate their financial status within a time period. It enables businesses to assess their financial performance in the past and helps them predict their financial standing in the future, allowing them to come up with and implement solutions to improve the way they manage their finances.

As a key business tool, a Profit and Loss Statement lets managers and owners keep track and view their sources of income and the allocation of their expenses. No matter the nature of a business and whether it sells goods or provides services, using this document provides a good idea of how a company is operating from a financial perspective.

In addition, by preparing and reviewing a Profit and Loss Statement periodically, it helps a business prepare its business tax return. Using the information from the statement as the basis for the calculation of net income, a company will be able to determine accurately the income tax it must pay.

Moreover, a Profit and Loss Statement can be used to show investors and creditors that it is beneficial to get on board with your business, as it gives them a quick overview or summary of the financial state of your company. The document is typically prepared by owners or accountants to be used by owners, finance officers, and shareholders to understand the state of a business. It may also be used by professionals to track their income and personal expenses to know if they are saving money or spending more than they earn.

How to fill out a Profit and Loss Statement?

The first step to filling out a Profit and Loss Statement template is to determine the period of time to be evaluated. In general, you can calculate for a month; nevertheless, you may evaluate on a quarterly, yearly, or even a weekly basis.

Below is a guide to help you fill out our Profit and Loss Statement Template.

The topmost part of a Profit and Loss Statement should show your company name. Provide your business address below the company name. Then, determine the period of time to be evaluated.

For the Income section, you can keep track of any money you are earning through sales of your products and services. If your company deals with the selling of products, provide the total sales amount on the Sales Amount field. For other income, including non-operation income such as rental or interest, provide the total amount on the Other Income Amount field. Compute for the Total Income Amount.

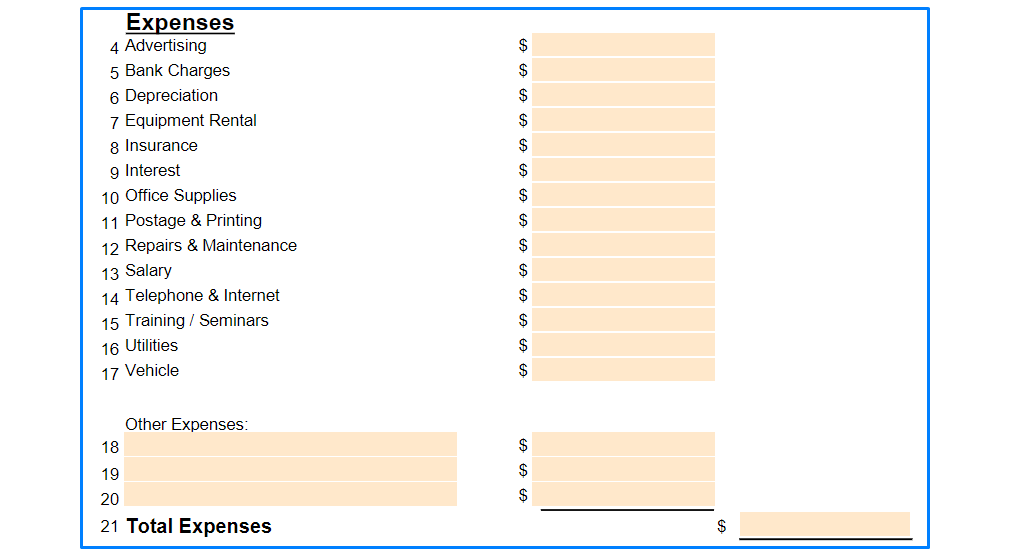

For the Expenses section, depending on the category of the expenses, provide the total amount of expenses on their respective field. If the expense falls under a category that is not listed, use the Other Expenses field. Compute for the Total Expenses Amount.

For the expenses, you may track your operating expenses and non-recurring expenses together or separately, whichever is easier for evaluation.

Once you have computed for the total amounts of the income and the expenses, subtract the Total Expenses Amount from the Total Income Amount to determine Profit or Loss.

Once you are done with the computations, write your name on the Prepared By field and the date you have completed the template.

Frequently Asked Questions About Profit and Loss Statement

What are profits in a business?

Profits in business are equal to the difference between total revenue and the total cost incurred in the production of goods and services sold. In order for a business organization to make a profit, it must produce enough revenue from the sale of its products to cover costs associated with the production and selling.

What is income in business?

In business, an income is defined as the amount of money that is brought into an organization by its regular operations. This means that the income must be recurrent, it should happen regularly, for example, several times a year. Income can also come in when you sell assets such as products and equipment or borrow money such as taking out a loan.

What do expenses mean in business?

Business expenses are defined as any reasonable and necessary expenses, which are directly related to the operation of a business. These include travel costs, employee training costs, employee uniforms, telephone bills, and equipment used exclusively in a business.

The key is that the expense must be both reasonable and necessary. Reasonableness is determined by looking at how similar businesses handle the situation in question: if all companies in a similar line of business incur an expense, it's probably reasonable for yours to do so as well. Necessity is established by demonstrating that your company needs this particular type of expense to operate successfully.

What is a loss in business?

A business loss is defined as a loss that is incurred in the course of normal business operations. For example, if you own a restaurant and your oven breaks down you could write off this expense because it is considered an ordinary and necessary expense for your business.

How do you calculate profit and loss?

You can calculate profit and loss by using the following formula:

Net Profit = Total Revenue (Profit) – Total Cost (Expenses)

In other words, if you have a list of costs and revenues for a given time frame, you can simply subtract the former from the latter to see how much money you made or lost.

What is the AP & L statement?

AP & L statement is a profit and loss statement. It is a financial statement that contains the estimated revenues and expenses of a company over a certain amount of time. It is used to determine the health of a company and it usually contains three sections: sales, expenses, and net income. Companies use a profit and loss statement to see if their business goals are being met. The statement lists the revenue or sales of a company and then subtracts all expenses to determine the profit or loss for a certain amount of time.

Oftentimes, people who work in corporations create these statements, but occasionally small businesses owners will create them as well.

How can I calculate profit?

To compute for the profit of a business, the formula is as such:

Revenue minus Cost of Goods Sold (COGS) minus Operating Expenses (OE) plus Interest Expense (INT) plus Other Income equals Net Income.

Revenue – COGS – Operating Expenses + Interest Expense + Other Income = Net Income

While this is correct 100 percent in that order, there are other factors to take into consideration when looking into the finance portion of the business. These factors include but aren't limited to start-up costs, taxes, and other income.

What is a profit account?

A profit account is an account where all the profit or loss items are posted in a journal. That means that when you record transactions in the Profit and Loss form, they will be posted to this account. It is a useful document to have as it shows you at a glance all the profit and loss items made in your business.

How do we calculate profit percentage?

To calculate profit percentage, you have to first find the amount of money you have made from selling a product. The amount of money you made is the price listed on the product, less the cost of that product.

If you bought a book for $20 and sold it for $25, your profit would be $5, since you would have made $25 from selling the book (its price) but only spent $20 to buy it (its cost). $25 - $20 = $5.

To find the percentage of profit, divide the total amount of profit by how much you spent initially to purchase the product: 5 / 20 = 0.25 or 25%. This means that for every dollar you spend on purchasing a product, your profit is 25 cents.

What is a total profit?

In financial terms, a total profit is a value that represents a positive change in the enterprise's net worth. It is indicated by the difference between income and cost.

In case of a total loss, on the other hand, this value will be negative. In this way, one can see that a company's economic situation should always be assessed from a long-term perspective. One must look beyond the current results to be able to estimate whether a company is profitable over time.

How do I calculate profit per unit?

To calculate profit per unit, you need to know your cost per unit. The formula is:

Profit per Unit = (Revenue – Cost) / Units Sold

For example, if you sell a widget for $5 and it costs you $2 to buy the material, then your profit on each unit sold would be ($5 – $2) / 1 = $3.

How do I calculate my revenue?

Revenue is the total amount of money you make from selling your product or service. You can calculate it by adding together all your sales for a given time period, such as daily, weekly, monthly, quarterly, or annually. More complex businesses use revenue projection models to figure out how much they will make in the next year.

How do I calculate the cost of my product or service?

Your cost is how much it costs you to produce your products or services. It includes both direct costs such as raw materials, wages, and equipment rental, as well as indirect costs such as rent for your business space, and insurance premiums. You can calculate the cost of your products or services by adding together the costs to produce each unit.

Is P&L the same as an income statement?

a profit and loss statement is not similar to an income statement although some of their items are the same. They also both display the financial performance and health of a business over a given period. The difference is that an income statement will report on earnings or losses for a company as a whole, while a profit and loss statement separates this reporting by divisions or departments inside the organization.

The P&L is focused on the results of each division or department, showing how profitable it was over a given period. It excludes the impact on earnings that might be caused by fluctuations in other divisions or departments, so if one division has significant losses, this will not affect the overall earnings reported on an income statement.

Since a P&L breaks out the results for each division or department, it is an important management tool. It provides a way to analyze and control profitability, as well as helping managers make decisions on how resources should be allocated within the company.

Most companies produce their own P&L reports internally, but they can also be found in public filings or on external websites.

The P&L Statement is also known as a Statement of Profit and Loss, Income Statement, Operating Statement, or Earnings Report.

How do you read a profit and loss statement?

To accurately read and understand a profit and loss statement, you must first understand the layout and structure of how it's organized. Moreover, you must also understand what each section consists of.

The purpose of a P&L is to assist management in making good decisions about the business by providing key financial information at different levels, including division, product line, and period-to-period comparisons. Moreover, because managers can monitor how well they are executing their plans through the P&L, the P&L statement is perhaps the most important financial document they will ever read.

A profit and loss statement contains sections that show sales revenue, expenses, and profits. Each section reports results for a different time period - for example, quarterly or yearly. In order to understand it, you must understand that the sections report results for different time periods and record information about sales, costs of goods sold, expenses, and profits.

Why are profit and loss statements important?

Profit and loss statements are important because they can tell members of a company what the financial state of the company is, how it achieved that financial state, and whether or not future investments in time or money would be wise. Although these statements will almost always contain positive numbers, other information may also be included to help other employees understand why certain decisions were made.

For instance, if a company experiences a net loss for the year, they may list the reasons why in their profit and loss statement. If this is the case, then other employees can see what went wrong and take that into consideration when restructuring their processes to improve overall profits.

The next step in reading a profit and loss statement is to determine if it has been presented in the order that it occurs during the year, or displayed in order of importance. The latter is often done for management reports because managers are usually more interested in the information at hand rather than how it gets there.

This means that while someone reading a management report may get to each section at their own pace, managers always read these sections in the listed order. If they are not presented in this way, then it is important to reorder them so that the information makes sense.

Revenue and expenses are always listed first on a profit and loss statement because they are what makeup whether or not there is a net gain or net loss at the end of an accounting period. If revenue exceeds expenses, then there is a net gain for that accounting period. If expenses exceed revenue, then there is a net loss for that accounting period.

The goal of every company is to make money, so when people are reading these financial statements they should be looking at the bottom line in order to determine if the company made any money. If the company did make money, then it is usually safe to assume that everything else in the statement makes sense.

If the company didn't make any money or lost some, then it's important to find out why. The reasons are listed in order of importance, so after finding this information people should look at what caused the largest loss or least profitable section.

For example, if the net loss is due to fewer customers making fewer purchases than expected it's important to examine why this happened. Did the company make an error in its advertisements? Did they promote the wrong products? Were their prices too high or too low compared with other companies' prices?

Finding these answers will help the company know what to improve in order to reach more people and hopefully make them want to shop at their store rather than at another's.

What should you look for in a profit and loss statement?

People should always look for trends in each section of a profit and loss statement. If one section is continually less profitable or has larger losses, then it may be time to cut back on some efforts. For example, if you are focusing on marketing so many different products to the same demographic of people, it may be time to broaden your sphere of influence or begin targeting some new customers altogether.

If a particular product is having issues selling, then it might be time to cut back on advertising for that product and increase advertising for another product instead. Be sure to use the data you have gathered about which products sell and which ones don't. For example, if wheat is selling at a higher rate than rice, then it might be wiser to decrease the amount of advertising for rice and increase ads for wheat because people may be going back to buying whole grains as a healthier alternative.

Using this data will help you to find the best budget that works for your company, while still making a profit. It may become necessary to increase marketing efforts in some areas and decrease them in others, but updates should always be made based on what was learned from data analysis.

Why do we need a profit and loss account?

A profit and loss account is needed to determine a business's success. There are two types of profit and loss accounts: a single-step income statement and a multi-step income statement.

The single-step method calculates each branch of the business, then adds them together to create an overall figure for the cost of goods sold, operating expenses, non-operating items, such as interest, and net income. This is the simplest form of a profit and loss account.

A multi-step method is more in-depth, breaking down sales, cost of goods sold, operating expenses, non-operating items, such as interest, and net income into smaller categories for each branch. For example, an owner could see how much money the company made from its product and how much was spent on raw materials for making the products.

The only major difference between the two types of profit and loss accounts is the depth of detail. A multi-step income statement shows more information but does not calculate as much aggregate data as a single-step income statement. While multi-step income statements are more detailed, the single-step method is more common due to its ease of use.

What is the difference between a profit and loss statement and a balance sheet?

The differences between a profit and loss statement and a balance sheet are probably more apparent to those who have been managing a business for years, but the novice entrepreneur learns pretty quickly that these two types of financial statements can be confusing even if they are enemies.

Profit and loss statements, also known as "P&L's", detail the performance of a business over a specific period of time, generally, one month, one quarter, or one year. They detail the revenue a company earned during that time as well as the expenses it paid to earn those revenues. If expenses were higher than revenues, then a loss was recorded for that period of time. If the reverse is true — revenues being greater than expenses — then a profit was earned during that specific period of time.

The other major financial statement a business prepares is the balance sheet, sometimes called a statement of condition. This financial statement lists assets, liabilities, and owner equity for a specific period of time, typically three to five years. Assets are items that are owned by the company, including cash on hand or money in bank accounts; accounts receivable — money that is owed to the company; and property, plant, and equipment — things owned by the company which has value. Liabilities are items that are owned by the company, including bank loans, accounts payable — money paid to suppliers or employees for services already rendered but not yet invoiced by the company, accrued interest on debt instruments such as notes payable, and accrued taxes. Equity or net worth is the amount of money that would remain if liabilities were subtracted from assets; it represents how much of the company's business value is owned by owners, not owed to others.

What happens if a business does not use profit and loss statements?

When a business does not utilize profit and loss statements, the consequences may be critical. A profit and loss statement is a necessity for any business because it provides a detailed look at how a company is performing. Whether you're a small business owner or a big corporation, it's important to understand why profit and loss statements are necessary.

What is the goal of profit and loss statements?

The goal of profit and loss statements is to help a company determine the health of its business. They allow a company to understand how much money is being made or lost by different aspects of the business. These reports also give managers an idea of how their initiatives are affecting the total productivity and efficiency of the company as a whole.

Why would a business want to use a profit and loss statement?

A business would want a profit and loss statement so that they can make decisions about how to run their business. A profit and loss statement can be a useful tool for people interested in learning more about a company's business practices, providing information on how well they are doing financially.

A profit and loss statement reports the revenues minus the expenses of a business over a specific period of time, usually one month or quarter. This income statement is also known as an operating statement or an "income and expense statement."

Do I need a profit and loss statement?

Your business needs a profit and loss statement if it has employees or contractors, sells products or services, uses a cash register, buys and resells inventory, keeps records using double-entry accounting, or files taxes using Generally Accepted Accounting Principles (GAAP).

Do loan payments go on the profit and loss statements?

Your business's profit and loss statement should only display the interest that you pay on your loans, not the principal.

How do you prepare a profit and loss statement?

To prepare a profit and loss statement for your business you need your business's information on its income and expenses for a specific period of time, usually one year. This statement shows how much income the business has generated from sales as well as how much money is spent to make those sales, and therefore whether or not the business made a profit. You must prepare all the financial information your company keeps to accurately create a profit and loss statement.

Keywords: profit and loss statement p & l statement profit and loss statement template profit & loss statement profit loss statement profit and loss statement sample profit and loss statement example

Copyright © 2025 pdfrun.com | Crystal Lake Media. All Rights Reserved.

Schedule a Product Demo

Talk to us and find out if PDFRun is a good fit for your organization.